Venue Owners, Event Organizers, and even Couples,

That hired mobile bar service probably is NOT insured, even if THEY think they are. Sure, the business has general liability insurance AND alcohol liability insurance – but that still doesn’t always mean you’re covered properly!

At the risk of ruffling a few feathers within the mobile bartending industry, we wanted to put this out there. Many, if not most, mobile bar services have an owner that holds an insurance policy, and will either “hire” 1099 independent Contractors/Bartenders OR will just bring on a few “under the table.” And that’s where the problem lies – and why you’re allowing uninsured or improperly-insured Bartenders to serve.

*note: if you’re a venue that doesn’t require insured bar services, or a homeowner that is just hiring a friend or someone off Thumbtack, I’ll cross my fingers for you, since that’s the only protection you’ve got.

Understanding the Basics: Employee Classification

First, it’s crucial to understand the difference between W-2 employees and 1099 independent contractors. W-2 employees are directly employed by the business, with taxes withheld from their paychecks, and they are covered under the employer’s insurance policies, including worker’s compensation and general liability insurance. On the other hand, 1099 contractors are self-employed individuals who contract their services to businesses. They are responsible for their own taxes and, crucially, are not covered by the hiring company’s insurance policies.

The Appeal of 1099 Contractors and Under-the-Table Payments

Many mobile bars and event services opt to hire Bartenders as 1099 contractors or even pay them under the table to reduce costs. This approach can initially seem beneficial for both parties: the business saves on payroll taxes, insurance premiums, and other employment-related expenses, while Bartenders might enjoy higher take-home pay. However, these short-term gains come with significant long-term risks.

The Insurance Illusion

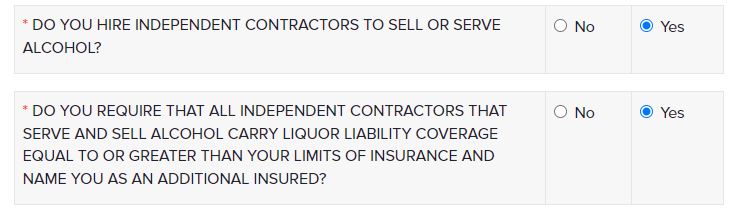

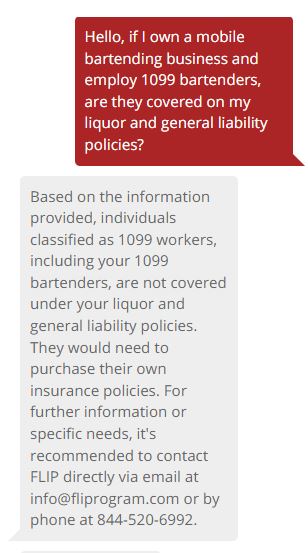

One of the primary concerns with hiring 1099 contractors or paying Bartenders off the books is insurance coverage. Mobile bar companies might have business insurance and even specific alcohol-liability insurance, but these policies often have a critical stipulation: they only cover W-2 employees. This means that if a 1099 Bartender causes an accident or serves alcohol to a minor, leading to an incident, the insurance policy will not cover the damages (see images of conversations we had with insurance providers below).

For venue owners and event organizers, this poses a significant risk. Even if the mobile bar company assures you that they have insurance and shows you their COI (Certificate of Insurance), if their Bartenders are not properly classified as employees, the insurance coverage can be voided. This leaves your venue vulnerable to lawsuits and financial liabilities, since the bar company probably doesn’t have a million dollars in their back pocket.

The Legal Repercussions

Imagine this scenario: during a high-profile event at your venue or home, a Bartender from a mobile bar overserves a guest, who then gets into a car accident on their way home. The injured parties sue the Bartender, the mobile bar company, and your venue. If the Bartender is a 1099 contractor, the mobile bar’s insurance might not cover the incident. Consequently, the venue or home-owner could be held liable for damages, resulting in substantial financial losses and reputational damage. When damages incur and financial responsibility are sought, the victim and their lawyers are going for the party where they’ll get the most money – especially if there is no insurance from the bar services. That’s typically the venue or home-owner.

In many jurisdictions, the responsibility to ensure proper insurance coverage can fall on the venue. This means that if a couple hires a mobile bar service, it’s imperative to verify not only their insurance but also the employment status of their staff.

Protecting Your Venue: Best Practices

To safeguard your venue from potential legal and financial fallout, follow these best practices when hiring mobile bar services:

- Verify Employment Status: Ensure that the Bartenders provided by the mobile bar are classified as W-2 employees. Request documentation to confirm this status.

- Check Insurance Coverage: Obtain copies of the mobile bar’s insurance policies and carefully review the terms.

- Request Additional Insured Status: Ask the mobile bar to add your venue as an additional insured on their policy. This can provide an extra layer of protection.

- Draft Clear Agreements: Many venues have a service agreement that vendors – especially catering and bartending – have to sign with general duties or rules (a few examples; cleaning the bar area at the end of the event, no shots allowed, liquor only for a certain time, etc.) so you can easily add the clause that all employees are legal W-2 employees and not 1099 Independent Contractors and/or “Under the table” and will provide proof if requested.

Case Studies: When Things Go Wrong

To illustrate the potential risks, consider the following case studies:

- The Charity Gala Fiasco: A high-end charity event hired a popular mobile bar service. The Bartenders, classified as 1099 contractors, failed to check IDs rigorously, resulting in underage drinking. When an intoxicated minor caused an accident, the ensuing lawsuit revealed that the mobile bar’s insurance did not cover the contractors, leading to the venue facing significant legal and financial repercussions.

- The Wedding Disaster: At a wedding reception, a Bartender from a mobile bar service slipped and fell, sustaining serious injuries. As a 1099 contractor, he wasn’t covered by worker’s compensation. He sued the venue for damages, arguing that the unsafe working conditions contributed to his injury. The venue faced a costly legal battle and settlement.

Conclusion: Due Diligence is Key

In the world of event management, the details matter. While mobile bars and stand-alone bartending services can add flair and excitement to your venue, ensuring that their operations are legally compliant and that their staff are adequately insured is paramount. The risks of hiring 1099 contractors or paying Bartenders under the table far outweigh the short-term cost savings.

By conducting thorough due diligence, insisting on proper employment practices, and securing robust insurance coverage, you can protect your venue from potential disasters. Remember, when it comes to hiring Bartenders for your events, cutting corners on employment status and insurance can lead to significant legal and financial consequences. Prioritize safety, compliance, and fairness to ensure that your events are not only successful but also secure.